The first step in the preparation of final accounts is the preparation of trial balance. So it is absolutely essential that we prepare the trial balance perfectly, so our final accounts do not contain any errors. Let us learn more about the methods and procedures of preparation of trial balance.

Browse more Topics Under Trial Balance

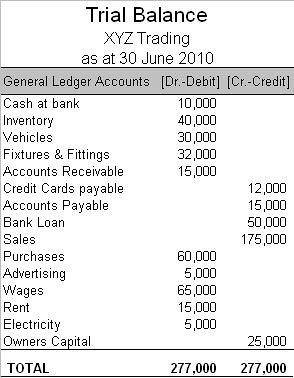

Trial Balance

A trial balance is a bookkeeping worksheet-like account that reflects all the credit and debit balances of all the ledger accounts. Once we prepare this statement, we can prepare the final accounts of the company on the basis of this trial balance.

One other important use of the trial balance is that it can determine the arithmetic accuracy of the accounts. So if both columns of the trial balance tally, we can be reasonably assured of the accuracy of the accounts. It does not ensure that the accounts are free of all errors but it can at least establish mathematical accuracy.

Preparation of Trial Balance

Preparation of trial balance is the third step in the accounting process. First, we record the transactions in the journal. And then we post them in the general ledger. Then we prepare a trial balance to verify that the debit totals equal to the credit totals. Let us take a look at the steps in the preparation of trial balance.

Learn more about Objectives and Limitations of Trial Balance here

- To prepare a trial balance we need the closing balances of all the ledger accounts and the cash book as well as the bank book. So firstly every ledger account must be balanced. Balancing is the difference between the sum of all the debit entries and the sum of all the credit entries.

- Then prepare a three column worksheet. One column for the account name and the corresponding columns for debit and credit balances.

- Fill out the account name and the balance of such account in the appropriate debit or credit column

- Then we total both the debit column and the credit column. Ideally, in a balanced error-free Trial balance these totals should be the same

- Once you compare the totals and the totals are same you close the trial balance. If there is a difference we try and find and rectify errors. Here are some cases that cause errors in the trial balance

- A mistake in transferring the balances to the trial balance

- Error in balancing an account

- The wrong amount posted in the ledger

- Made the entry in the wrong column, debit instead of credit or vice versa

- Mistake made in the casting of the journal or subsidiary book

Rules for Preparation of Trial Balance

While preparation of trial balances we must take care of the following rules/points

1] The balances of the following accounts are always found on the debit column of the trial balance

- Assets

- Expense Accounts

- Drawings Account

- Cash Balance

- Bank Balance

- Any losses

2] And the following balances are placed on the credit column of the trial balance

- Liabilities

- Income Accounts

- Capital Account

- Profits

Solved Question on Preparation of Trial Balance

Q: What are the two methods of preparing the trial balance?

Ans: There are broadly two methods for the Preparation of Trial Balance. They are

- Total Method: Here the totals of the credit and debit columns of the ledger accounts are transferred to the Trial Balance. The closing balance is of no concern

- Balance Method: Here only the closing balance is transferred to the Trial Balance on the relevant credit or debit column.

Leave a Reply