Trading account is a statement which is prepared by a business firm. It shows the gross profit of business activities during a specific period. It is a part of the final accounts of the entity. In other words, the trading account gives details of total sales, total purchases and direct expenses relating to purchase and sales. Trading account format for the year contains Particulars, Amount, Dr., Cr., Purchases, Sales, etc. In this article, we will see the advantages of a Trading account and Trading account format.

Trading Account

Trading and manufacturing business firms deal in sales and purchases of goods. Therefore, only manufacturing and trading entities prepare the trading account. Service providers do not prepare this.

Advantages of Preparing Trading Account Format

- It is a very important statement from the cost point of view of the goods. By preparing the Trading account entities can take the decision for continuing or discontinuing a particular product. It helps to earn the maximum profit or reduce the losses.

- With the help of a trading account, Sales tax authorities can easily see the correct purchases and correct sales as per the sales tax return submitted by a business firm.

- It also helps the Excise authorities to assess the excise duties of business firms.

- The management decides the price of the product with the help of a trading account, after keeping in mind the market competition.

Understand the Concept of Profit and Loss Account here in detail.

Items in Trading Account Format

Trading Account contains the following details

- Opening stock details of raw material, semi-finished goods and finished goods.

- Closing stock details of raw material, semi-finished goods, and finished goods.

- Total purchases of goods fewer Purchase Returns.

- Total sales of goods fewer Sales Returns.

- All direct expenses related to purchases or sales or manufacturing of goods.

Items of Income (Cr.) side

- Total sales of goods fewer Sales returns

- Closing stock of goods.

Items of expenditure (Dr.) Side

- Opening stock of goods

- Total purchases of goods Less purchase returns

- All direct expenses like Carriage inward & Freight expenses, Rent for godown or factory, Electricity and Power expenses, wages of workers and supervisors, Packing expenses, etc.

Notes

- The Trial balance never shows the Closing stock. However, firstly, we need to show the amount of closing stock on the income side of Trading account and secondly, in the balance sheet under current asset.

- We value the closing stock at cost or market price, whichever is less.

- On the date of preparation of trading account, we value the Closing stock which is physically available.

- However, we can prepare the Trading account in horizontal form also but the contents shall remain the same.

Trading Account Format

| Particulars | Amount | Particulars | Amount |

| To opening stock | By sales | ||

| To purchase | Less: Returns | ||

| Less: returns | By Closing stock | ||

| To direct expenses: | |||

| Freight & carriage | |||

| Custom & insurance | |||

| Wages | |||

| Gas, water & fuel | |||

| Factory expenses | |||

| Royalty on production | |||

| To Gross profit c/d | |||

Solved Example For You

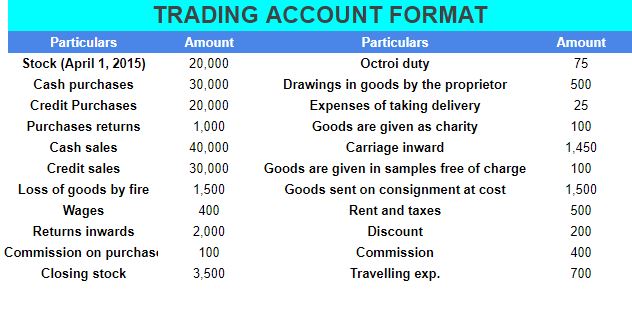

Prepare a trading account for the year ending March 31, 2016, from the following particulars:

| Particulars | Amount | Particulars | Amount |

| Stock (April 1, 2015) | 20,000 | Octroi duty | 75 |

| Cash purchases | 30,000 | Drawings in goods by the proprietor | 500 |

| Credit purchases | 20,000 | Expenses of taking delivery | 25 |

| Purchases returns | 1,000 | Goods are given as charity | 100 |

| Cash sales | 40,000 | Carriage inward | 1,450 |

| Credit sales | 30,000 | Goods are given in samples free of charge | 100 |

| Loss of goods by fire | 1,500 | Goods sent on consignment at cost | 1,500 |

| Wages | 400 | Rent and taxes | 500 |

| Returns inwards | 2,000 | Discount | 200 |

| Commission on purchase | 100 | Commission | 400 |

| Closing stock | 3,500 | Travelling exp. | 700 |

Ans:

Trading Account

(For the year ending 31st March 2016)

| Particulars | Amount | Particulars | Amount | ||

| To opening stock | 20,000 | By Goods sent on consignment a/c | 1,500 | ||

| To purchase | By sales | ||||

| Cash purchase 30,000 | 30000 | Cash sales | 40000 | ||

| Credit purchase 20,000 | 20000 | Credit sales | 35000 | ||

| Less: Return outward 1,000 | (1000) | Less: Return inward | (2000) | 68000 | |

| Drawings 500 | (500) | ||||

| Goods as charity 100 | (100) | ||||

| Goods as sample 100 | (100) | 48300 | |||

| To carriage inward | 1,450 | By P&L A/c (Loss by fire) | 1,500 | ||

| To wages | 400 | By closing stock | 3,500 | ||

| To commission on purchases | 100 | ||||

| To Octroi duty | 75 | ||||

| To Expenses of taking delivery | 25 | ||||

| To Gross profit transferred to P.&LA/c | 4,150 | ||||

| 74,500 | 74,500 |

Leave a Reply